After very strong growth in Q1, the Australian economy is entering a period of slightly below trend growth of between 2.5% and 3.0%. This means that RBA is likely to retain its neutral policy stance. Moreover, recent communications from RBA Gov Stevens highlighted the probable intention to not cut rates saying „cumulative movements in interest rates since the start of the year amounted to a noticeable easing in financial conditions‟ and that he does not think that „lower rate is the answer‟. As a result, we believe that unless we see big surprises in the incoming data, domestic factors a not likely to be the main drivers of AUD in coming months.

As shown previously, the AUD is likely to be driven by two factors: 1) the outlook for US yields and its impact on flows into AUD assets; and, 2) the needed convergence of the AUD toward weaker commodity prices. As such, a model linking the value of the AUD to relative prices, commodity prices, rates differentials and risk appetite, suggests that the AUD should trade around 0.85.

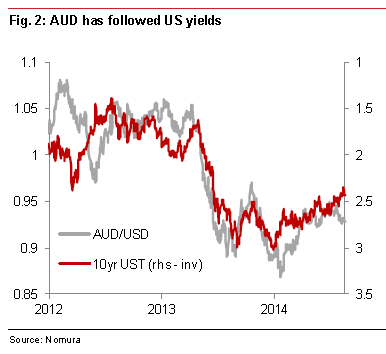

Recent US indicators continue to point to a strengthening of the economy. After contracting in the first quarter of 2014, the US economy rebounded significantly in Q2, suggesting that growth should stay robust in the second half of this year. Moreover, thelabour market continues to remain strong, with strong jobs gains and initial jobless claims suggesting further improvement in the labour market. Moreover, inflation has edged higher recently, while wages remain softer. All this is pointing to a Federal Reserve that should sound gradually hawkish, which should push Treasury yields higher and the USD with it. Also, as shown in Sore Spots in FX, the AUD is very sensitive to increases in US short term rates.

As a result of expected higher US Treasury yields, we expect to see downward pressures on the AUD developing in the coming months. The higher US yields will make it less attractive for foreigners to invest in Australian assets. Moreover, a depreciation in the currency would also mean weaker returns or even loses on foreigners‟ holdings of AUD assets, which would also reduce the inflows.

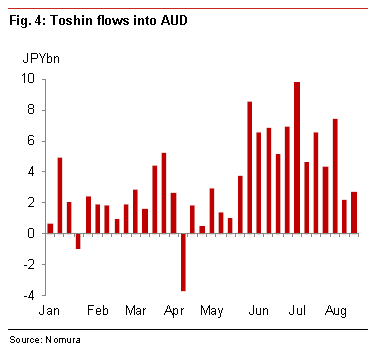

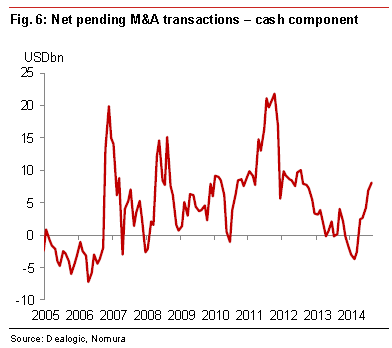

However, continued M&A related inflows could provide some support to the currency. As result, we expect the AUD to gradually depreciate for the rest of the year, and even end the year slightly below 0.90.

Fair enough. I have only one bone to pick. US yields are not rising even though the prospect of a rate hike is now very firm. This is largely because despite improving US growth, inflation is quiescent and will likely remain so. Growth will hold permanently below 3% (secular stagnation) as any credit recovery will remain subdued and global commodity prices keep falling on the Chinese adjustment.

The world is in a position today to play one giant pair trade on US equity and bonds and that means the closing of the interest rate spread with Australia is going to be painfully slow, until the RBA cuts again as the terms of trade keeps plunging.

Then again, the Nomura is hardly calling for the dollar to fall out of bed so it’s probably near the mark.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.